For any large industrial base, a major barometer for potential output and manufacturing sophistication is the installed base of machine tools. These are a broad category of industrial machines used to cut, shape, and form components that are subsequently assembled into finished products. While forging involves applying pressure to deform material and casting involves pouring molten material into moulds, machining primarily consists of cutting and refining solid material into precise components.

Having greater access to machine tools, whether on one’s own production line or distributed across suppliers, reduces lead times, increasing potential output as well as lowering long term borrowing costs. Machine tools used in advanced weapons production, such as guided missiles, tend to be specially configured and are designed for relatively small orders. In Britain, parliamentary discussions stretching back to 1951 revolved around ministers assuring their opposition that Britain had an adequate machine tools base to rearm after World War Two.

Russia’s invasion of Ukraine and the ongoing Iran War and its significant rearmament have shown the importance of machine tools. Access to off-the-shelf, militarily applicable chips has proved incredibly easy in the modern economy. Russia, Ukraine and Iran are all able to access, operate and dispense millions of chip-dependent systems despite having very little domestic fabrication capacity themselves.

The ability to install and operate advanced machine tools to manufacture advanced military components is far more challenging. Even the mighty Chinese industrial base has struggled to gain a manufacturing presence in the high-end machine tool market, with European and Japanese producers still dominating at the cutting edge. While China can supply Russia with large numbers of machine tools, the latter still seeks to evade sanctions and access the most advanced Western equipment.

After the fall of the Soviet Union, Russia’s defence industrial base fell into a long period of decay. By the time Putin began rearmament, the skilled machinists responsible for producing key military components had either retired or died. The machine tool industry had also evaporated. In 1990, the Soviet Union was the third largest machine tool producer, making around 25,000 annually. These were generally more numerous and less sophisticated than modern-day machines. Nowadays, Russia is producing well under 1,000 machine tools.

Slowly, Russia has been rearmed through the importation of machine tools, most notably computer numerical control (CNC) machines. Russia has subsequently spent huge sums importing machine tools to improve its war-making capacity, initially from Western countries but increasingly from China. The various missile and military equipment plants dotted around Russia are, for the most part, machining centres, turning metal into key components that meet specific performance thresholds.

As the Russian example shows, access to the very best machine tools, either through domestic production or imports from friendly states, is clearly a first-tier military issue. But besides this, a large machine tool installed base impacts the pace of production in commercial industry. British policy makers, when thinking about industrial policy, should consider the supply and investment in machine tools a high priority.

By and large, they have not, and the stakes of inaction are high. If British leaders double down on industrial policy without focusing on the key importance of machine tools in improving overall capacity, they are likely to discredit attempts at reindustrialisation altogether. The scheme is made necessary by the urgency of the problem. From 2000 to 2024, Britain’s heavy industry almost halved in terms of value. Long periods of stagnation are increasingly interrupted by global shocks which always work to our disadvantage. The current Iran war has led to the highest increase in input prices for British manufacturers for decades. The situation is so desperate that some are tempted to throw up their arms and say Britain should not try to restore manufacturing power—instead doubling down on services. This would be a mistake. Besides the direct link between manufacturing and military capability, Britain is economically stagnant due to low productivity and a lack of presence in new industries. Some significant recovery in manufacturing is not just in the national interest, but also in the commercial interest.

This paper proposes the Machine Tool Finance Corporation. This will be a small team of manufacturing experts sitting under the National Wealth Fund, which will be responsible for providing grants for machine tool purchases across the UK. The grant scheme will have an annual budget of £1 billion, and will run for a single parliamentary term after which its impacts on investment and productivity can be scrutinised. Most of the money will be directed towards the purchase of capital equipment, but as the scheme progresses, it will slowly dispense funds to improve domestic machine tool building capacity.

Machine Tools: What They Are

Industrial manufacturing depends on a range of processes requiring specialised equipment. Casting involves pouring a liquid into a casting die usually formed from sand, which then cools and solidifies to form a desired shape. Forging, another key manufacturing process, involves compressing or extruding metal with a specialised press. Huge forge presses are required to stamp and shape large steel alloy ingots for metal structures like pressure vessels.

Machining is the process of shaping a desired form by removing excess material and is essential to the fabrication of the vast majority of durable goods components. This is served by machine tools, which range in sophistication from manually operated mills and lathes to advanced computer numerical control (CNC) machines. Machining is considered “subtractive” manufacturing, as it removes material to create a desired shape or characteristic. “Additive” manufacturing and 3D printing are defined against these more established processes.

Machine tools are a broad term. They invariably involve a workpiece, which is reduced by a cutting tool. For lathes, the workpiece rotates while the cutting tool is stationary, making them ideal for making cylindrical shapes. For milling machines, the opposite is true, making them ideal for flat and complex shapes. There are also broaching, grinding and boring machine tools. Altogether, these machines are the bedrock for the production of fabricated metal components.

No one major machine tool producer owns more than 5% of the global market. While there are many machine tool vendors, they are largely concentrated in a handful of what we might call industrial specialist countries—Germany, Japan, Switzerland, Italy, Korea and Taiwan. China and the United States, by virtue of their sheer size, have significant machine tool production in their own countries.

Britain is a relatively minor actor in the machine tool space. We were the original market for such tools. In order to mass-produce pulley blocks for the Royal Navy, Isembard Kingdom Brunel procured specialist machine tools from the toolmaker Henry Maudslay. Between the late nineteenth century and late twentieth century, the home of British machining was Coventry, the big four makers being Webster & Bennett, Alfred Herbert, Coventry Gauge & Tool (latterly known as Matrix Churchill), and A C Wickman.

British machine tool makers were generally slow to adopt numerical control machines, first developed by the Americans. And when they did, companies like Alfred Herbert stubbornly made their own electronic equipment, despite this being far beyond their core competency. The various companies often fell under foreign ownership with mixed results. Matrix Churchill, in the 1980s, became controlled by Iraqi interests, and with the secret blessing of the British government, exported high-end machine tools to Saddam Hussein during his war with Iran.

Today, we are much more limited, producing about £600 million worth of machine tools every year. Britain’s most notable machine tool-adjacent company is Renishaw. Founded in 1973, it is now a publicly owned company that is known for making measuring instruments for machine tools. It also makes 3D printing machines. For the most part, it is selling components to large machine tool manufacturers, with its most important market being East Asia. There are other niche makers of UK machine tools, but they are marginal. Most machines are imported. As an example, Goodwin International is a major fabricated metals company in Stoke. It lists its milling machines and lathes based on their make and manufacturer, with almost all of them being Japanese or Korean.

It is worth separating machine tools from robots, as the two are often used interchangeably. Broadly speaking, machine tools are more fundamental to industrial capacity. Most industrial robots perform machine tending, machine handling, assembly, packaging, or welding. They are, for the most part, not cutting or forming material into specific components. Mobile robots are mainly doing transportation and material handling work, with a growing number doing cleaning. According to the IFR, in 2024, 47% of industrial robots went into electronics and automotive. Robots are often best justified in bulk, and the whole production line has to be built to accommodate them.

Machine tools, on the other hand, are the atomic unit of production. What ultimately determines lead times is how much metal can be cut and formed and to what specification. Machine tools improve a manufacturer’s throughput potential and enable companies to machine a wider range of products, including those requested sparingly. While robots can automate certain parts of production and render huge productivity improvements, machine tools are critical for actually expanding production capacity. Policymakers interested in reindustrialisation should therefore prioritise machine tools over robots.

The Real UK Manufacturing Problem

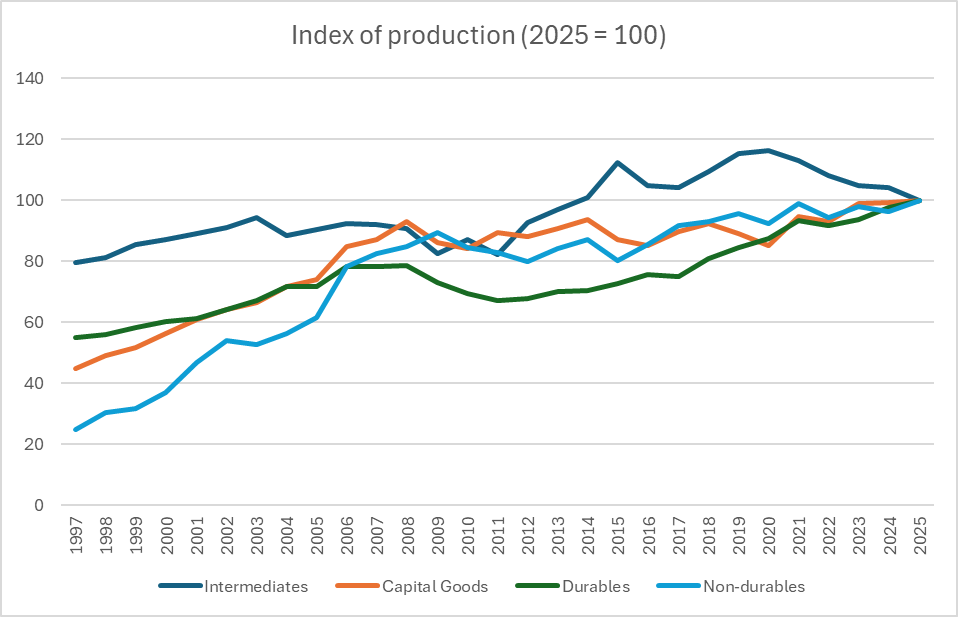

We can look at the index of production for different sectors to see where the UK manufacturing base is strong and weak. The industrial base can be split into four segments: Intermediates are unfinished components that pass through the supply chain. Finished goods, including durable and non-durable goods, are sold to customers, and capital goods are machines that convert intermediates into more refined intermediates and finished goods.

Intermediate goods production is one of the best measures of industrial capacity because, in addition to covering crude steel and basic heavy goods, it also includes low-volume, high-mix fabricated products. Examples would include turbine blades and engine casings for aircraft, braking systems for locomotion, bespoke pump systems for industrial machinery to name a few. As shown, post-COVID intermediate goods production has declined. The most obvious reason for this is the decline of energy-intensive primary goods production due to high gas and electricity costs.

Capital goods production, which includes machinery, aircraft engines and transport equipment, has barely budged since 2008. The great over-performer in British manufacturing has been non-durables. This includes food, fuel, pharmaceutical products, clothing and household cleaning products, among other things.

Figure: Index of Production for different categories of manufacturing products. Source: ONS.

From this, combined with what we already know about Britain’s low stock of plant equipment and low shipments of robots and machine tools, we can argue that Britain’s primary deficiency lies in intermediate production. Some of this is due to energy prices causing havoc in metals, inorganics and chemical products. But a lot of it is deficiency in machine tool capacity.

There are two main types of intermediates. There are primary intermediates that are refined from raw materials. Here, a plant is turning one or a handful of ingredients into a wider range of products. Crude oil is segmented into gasoline, naphtha, diesel and kerosene at refineries. Crude iron and scrap are melted down to produce crude steel. Proteins are packaged into food products. Britain has struggled in this sector because of energy prices.

The secondary intermediate market is less reliant on energy and more reliant on machine tool capacity. If you have more machine tools, and by extension more qualified machinists, you can get your primary intermediates refined further and sent to assembly plants where they can be turned into either capital goods or durables. While British primary intermediates have been hammered by energy prices, secondary intermediate production is bunged up by a lack of machine tools.

The Decline of British Capital Equipment Spending

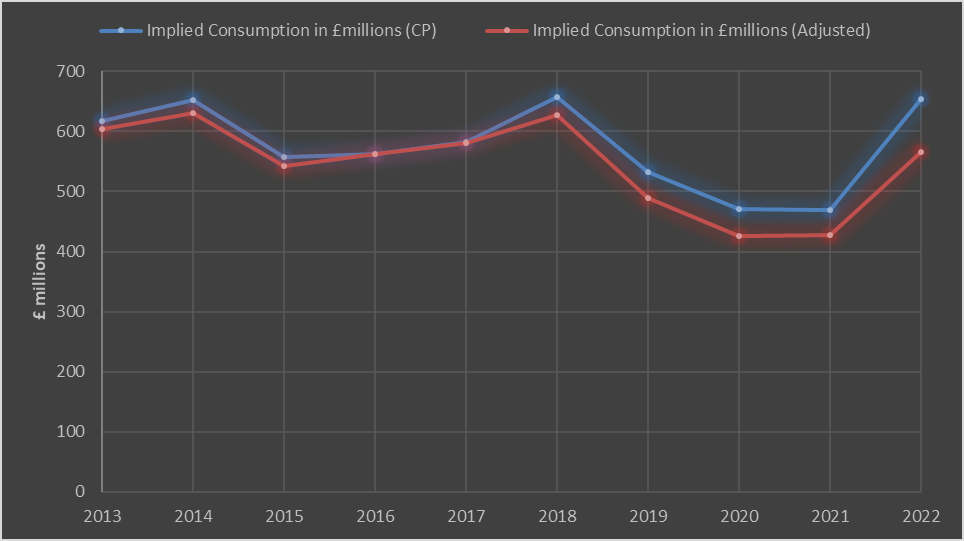

We can see the drop in UK capital equipment spending through the machines themselves. From 2013 to 2022, data from the Manufacturing Technologies Association (MTA) indicate that British machine tool consumption was static or declined in real terms. While up-to-date estimates are limited, in 2025, the MTA estimated that machine tool consumption declined by 10% from 2024.

Figure: UK machine tool consumption in £millions per year. Source: CECIMO.

It is worth pointing out just how little we spend on machine tools every year. We spend less than £1 billion on purchasing the systems themselves every year (not accounting for parts and installation).

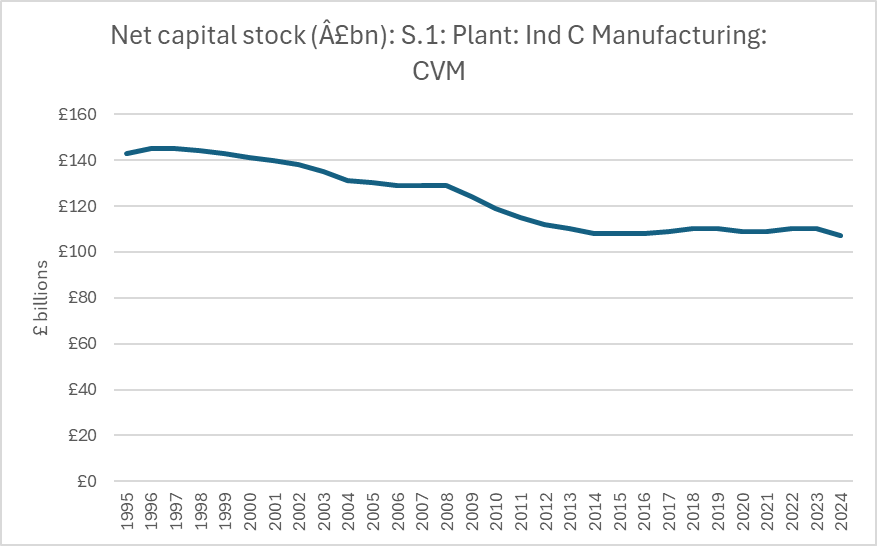

Low machine tool spending exemplifies a larger drop in investment in British manufacturing that goes back decades. We can see that, since 1995, on an inflation adjusted basis, the net capital stock value of plant equipment for British manufacturers has actually declined. Where there has been capital stock growth, it has been in intellectual property and software. The real value of plant and machinery in British factories in 2024 was just 75% of what it was in 1995. While capital stock and industrial capacity are not perfect analogues, they are pretty good proxies for each other.

Figure: Net capital stock for plant and industrial equipment in manufacturing, 1996 to 2024. Source: ONS.

Plant equipment, including machine tools, piping, robots, and other equipment, accounts for a large share of manufacturing capital spending, and to a great extent determines longterm industrial capacity improvements. That there is so little investment is a bad portent for long-run British manufacturing.

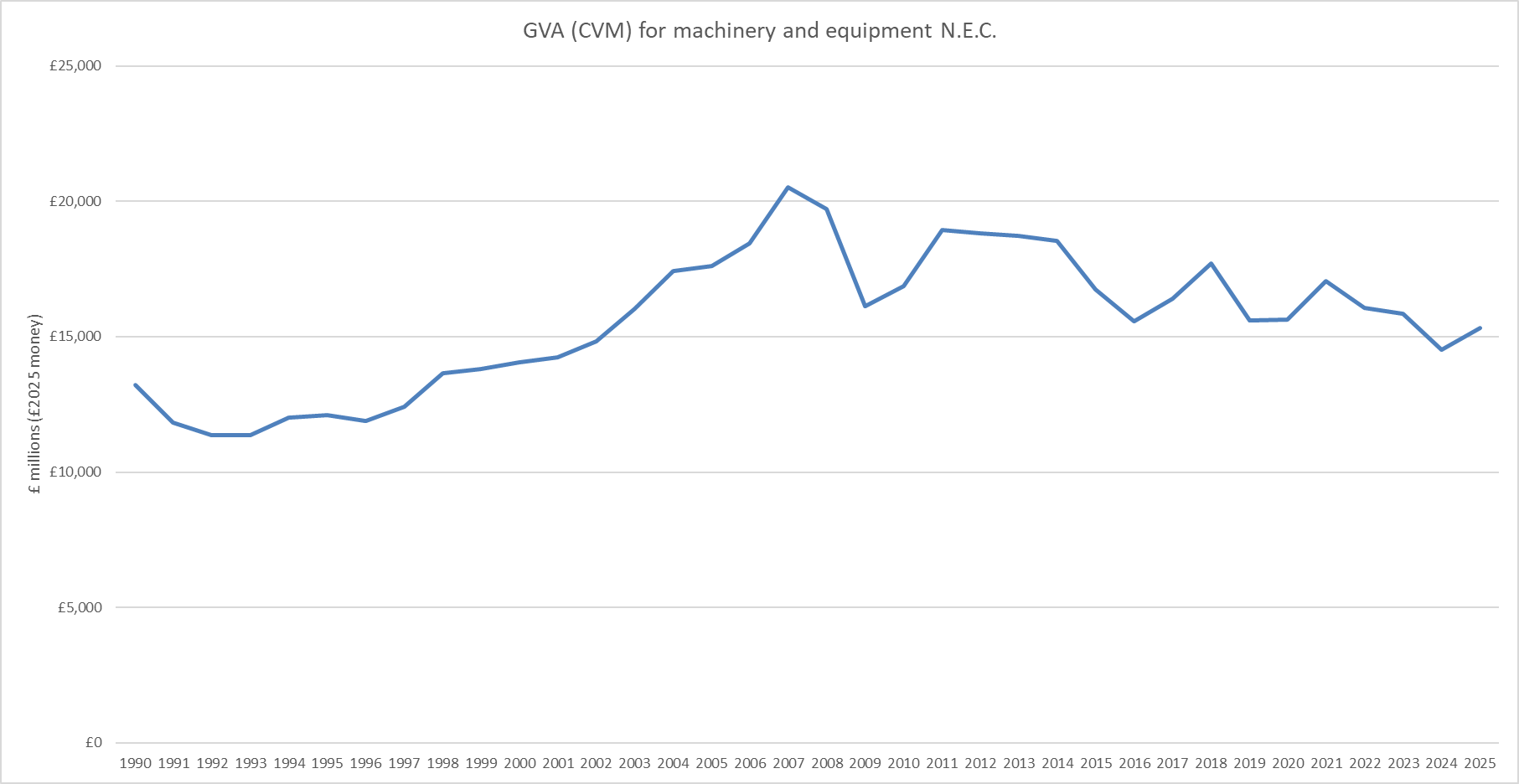

We are not just buying fewer machine tools. We are making fewer and using them less. When looking at machinery revenues related to machine tools, recent years have seen a clear decline in the level of gross value added (GVA) data. From 1990 to 2025, inflation-adjusted GVA for machinery and equipment (which includes machine tools) peaked in 2007.

Figure: GVA (£2025 millions) for machinery and equipment N.E.C.

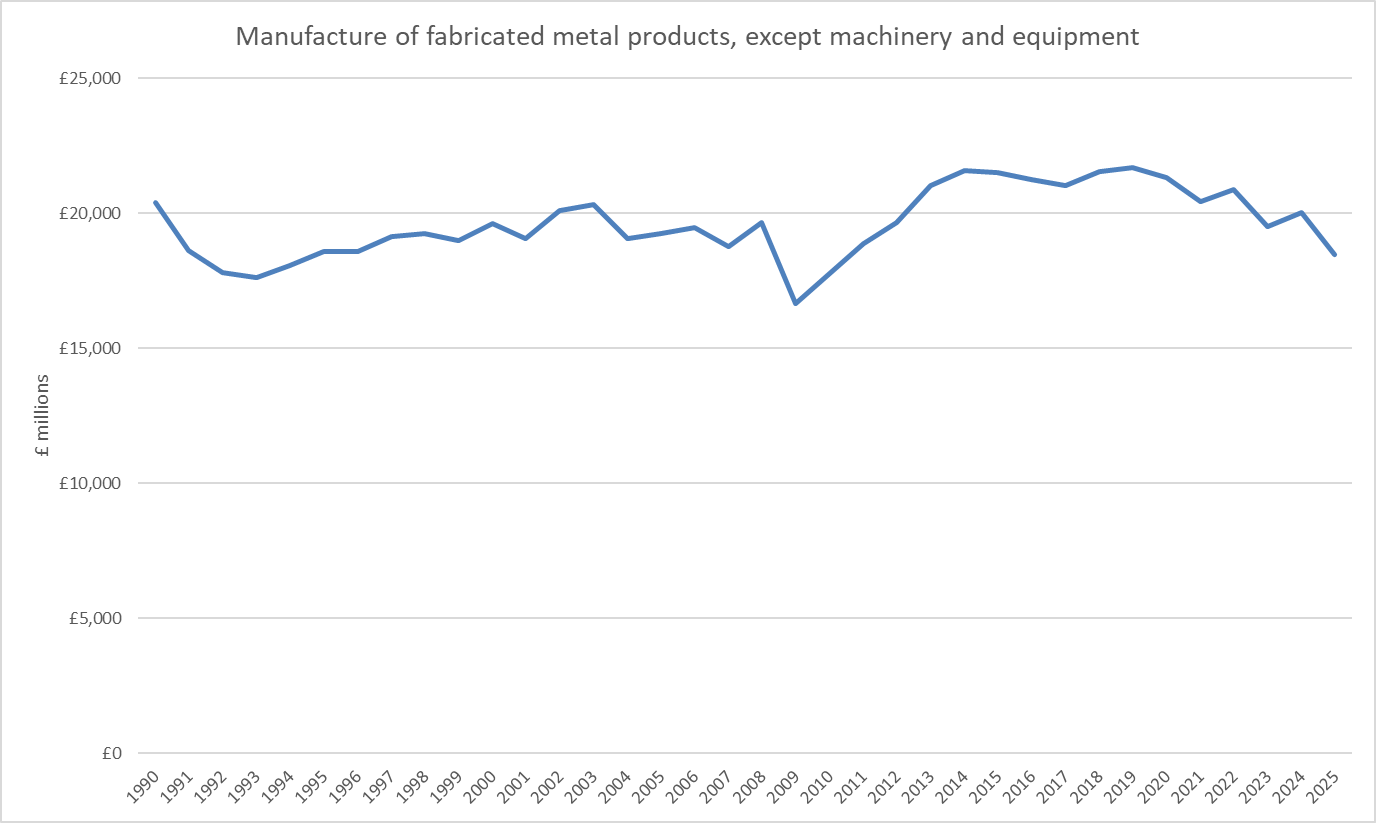

The kind of activity machine tools are used for, namely, manufacturing fabricated metal products, has been declining for some time.

Figure: GVA (£2025 millions) for Manufacture of fabricated metal products, except machinery and equipment.

Why does the UK struggle to finance machine tools? The costs of such equipment are usually high relative to the buyer’s outlays. A 5-axis CNC machine costs anywhere between £300,000 and £800,000. Lenders of capital tend to demand significant deposits up front (20-30%), and demand short payback periods.

The machine shops themselves are structurally small. They often specialise in a few products for a handful of local customers, and do not make sufficient margins to acquire smaller operations. What is more, there are no easy economies of scale in machining. Scaling is largely linear and determined by the number of machines multiplied by the utilisation rate, which is often hard to control due to uneven orders.

There are machine shops that have scaled—they are the electronic contract manufacturers of East Asia, like Foxconn, Pegatron and BYD Electronics. Like machine shops, they fabricate components for businesses, in their case, electronic components for computer equipment. But because the components market for electronics is so large, their economies of scale are much larger. Even then, ECMs like Foxconn have very small net margins of well under 5%. Therefore, they are only able to thrive in East Asia, where such a business can find adequate financing.

Despite this, machine shops in Europe and the U.S have fared moderately well, while in Britain they have stagnated. Fundamentally, Britain’s industrial base is dominated by foreign firms, suffers from bad regulation and crippling energy prices, and every government decision suggests that Britain is not planning to be a manufacturing power of note in the long term. This needs to change.

The Machine Tool Finance Corporation

Currently, machine tool finance can be supported through full expensing, which, since 2024, has allowed the purchase cost of capital equipment to be fully deducted from corporate tax in the first year of purchase. Full expensing was introduced to replace the super-deduction programme, a post-COVID measure to stimulate investment.

The super-deduction involved a 130% deduction of a capital purchase from a 19% tax rate. There was a short-term increase in robot shipments due to the super-deduction, and this likely also applied to machine tools. It is worth noting that the super-deduction did not provide significantly greater relief than free-expensing. A 130% deduction at a 19% corporate tax rate and a 100% deduction at a 25% tax rate yield essentially the same effective saving of 25%. Nevertheless, the shift from super-deduction to full expensing increased the overall corporate tax rate by 6%, thereby reducing investment. Given where we are, it is unlikely that tax credits alone are sufficient to boost machine tool growth.

There is another way to support machine tools: loan guarantees. Since 2024, the Government has supported small businesses in making large investments through the Growth Guarantee Scheme (GGS). Here, the government guarantees up to 70% of a £2 million loan for qualifying small businesses.

Isembard, a start-up, has proposed expanding the GGS specifically for machine tools and industrial assets. This would involve the government guaranteeing 90% to 100% of the loan instead of 70%, and mandating lenders to offer low initial deposits and provide generous payback terms of 10 years, also suggesting fixed interest rates.

This is a good idea. However, lenders can still refuse such terms. While loan guarantees are certainly welcome, the funding gap in British manufacturing likely makes them insufficient. Given the dearth in investment and the decline of the capital stock in industry, we need the policy equivalent of a bazooka.

The proposal is for a £1 billion support programme to support machine tool spending, running annually for a five-year parliamentary term. Three-quarters of the spending (£750 million) would be for machine tool grants, more than doubling the purchasing power of UK industry. The remaining quarter would provide grants to machine tool makers to set up UK branches with at least some machine tool production capacity. The funds could be handled via the National Wealth Fund.

Why prioritise purchases over domestic machine tool manufacturing capacity? After all, the national security importance of machine tools suggests that it would be preferable if UK plc could make its own. To this, I respond that you have to learn to walk before you can run. The UK is starting from a very low level of capacity. It will take time to scale up machine tool manufacturing. These are complicated systems that only a handful of countries produce at any significant scale. By contrast, it will take considerably less time to import machine tools into the UK. The immediate aim is to increase the nation’s overall productive capacity, with domestic machine tool manufacturing being an important but secondary objective.

The scheme would not discriminate based on a company’s size, but would limit the number of machine tools per grant receiver. Anyone who sold the equipment in the next five years would have to repay the grant. The government would be able to assess the utilisation of the tools for which it provides grants and ensure this subsidy is not squandered.

It could be argued that this proposal is similar to a grant system that ran under the Labour government of 1966 to 1971, which had decidedly mixed results. Here, grants providing up to 20% of funding for different industrial projects were managed by the Industrial Reorganisation Commission (IRC).

In their first year, these grants totalled £432,000 of funding for 33 projects. This is about £7 million in today’s money. The annual outlays had grown enormously to around £500 million, or £6 billion in today’s money, by 1971. On scrapping the grant programme, the Tory government of 1971 thought it could save £1500 million between 1970 and 1975, or £20 billion in today’s money. The scheme then reached an annual subsidy of around £5 billion annually in modern money.

The investment grants of the sixties were certainly far larger than what is proposed here (£5 billion in a parliamentary term). Did they succeed? They certainly led to capital deepening. Between 1966 and 1973, industrial production grew 24% in real terms. There were problems, of course. The grants, though large, were not particularly focused and were linked to other government objectives, such as mergers and the reduction of regional disparities by incentivising manufacturing in poorer regions. Grants were prioritised in development areas for instance. For a machine tool grant scheme, there would be no such focus.

Why would a limited reintroduction of grants be a good thing? Firstly, this is more limited in scale as a share of GDP, but also more focused on one particular class of equipment, in an area where Britain is clearly deficient. It targets the intermediate stage of production, where Britain is weakest. The comparisons to 1966 are also limited. Back then, British industry was relatively wasteful and was less exposed to global competition. Today, the British manufacturing base is among the least protected in the world, either from tariffs or subsidies. For instance, the UK has not followed the U.S. or EU in putting tariffs on Chinese electric vehicles. It has suffered decades of real decline in net capital stock for machinery. The impetus for targeted intervention is therefore much greater now than it was then.

The machine tool scheme will cost just £5 billion over five years. This is similar to the funds targeted for advanced manufacturing in the 2025 industrial plan, which earmarks £4.3 billion in spending between 2025 and 2035, including £2.8 billion in R&D funding up to 2030. This can be quickly offset by making economies elsewhere.

For example, the government could cut back on research tax credits, which cost the Exchequer around £7.5 billion a year. Alternatively, the Renewable Obligation Certificate (ROC) scheme, the zombie subsidy for expensive intermittent technologies that was brought in before the financial crash, costs over £7 billion annually. Feed-in-tariffs, another subsidy for small solar generators, cost nearly £2 billion a year. The government has also earmarked £21 billion in carbon capture and storage over 25 years, or £840 million a year. Subsidies to get people to install heat pumps cost nearly £700 million in 2025.

Overall, the UK spends about £60 billion in tax credits, loan guarantees and grants every year, nearly 3% of GDP. Very little of it is focused, and much of it is ripe for cuts. On top of this is the £14 billion spent on foreign aid. Ultimately, we can juice the British industrial base and increase our defence manufacturing capability by focusing grants on one major bottleneck.

Conclusion

The remaining three quarters of the 21st century are likely to be more turbulent than the first quarter. We can see that ambitious and revanchist countries, from Saddam Hussein’s Iraq, to Putin’s Russia, to China, have prioritised advanced machine tools as a way to industrialise and also to expand their military capacity. Britain is clearly deficient in manufacturing, having not grown its industrial base for decades. By some measures, like the value of our installed plant equipment, our industrial base is actually considerably smaller than it was in the 1990s. Our machine tool installed base is small compared to Western and East Asian counterparts, and directly contributes to our inability to manufacture quickly and at scale. This greatly limits potential military capacity, which is increasingly being defined by large numbers of expendable munitions.

Given the chronic underinvestment of machine tools in the UK, it is time to shift simply from incentive schemes like tax credits towards grants for equipment spending. The scheme is targeted and the outlays of £1 billion a year are not excessive, but are still enough to drastically expand purchases immediately. It could be easily funded through cuts to frivolous industrial policy spending, especially related to the subsidising of heat pumps or subsidies for building offshore wind. While grants for machine tools would have to be combined with other supply-side related reforms to induce a genuine manufacturing renaissance, the scheme itself would rapidly reduce lead times for a huge range of advanced components and make manufacturing in Britain in general more attractive. The cost of inaction is also high, with many machine shops struggling to replace equipment, and often closing down due to owners retiring. The case is clear: stop talking about reindustrialisation and start furnishing the factories with the machines that can make it happen.